Executive Summary

In the ever-evolving landscape of commercial real estate, one asset class has emerged as the undisputed champion of risk-adjusted high yielding returns: Small-Bay Industrial Real Estate. While institutional investors have historically fixated on bulk distribution centers and trophy office towers, the humble small-bay warehouse—typically defined as industrial properties under 200,000 square feet with individual tenant suites ranging from 1,000 to 10,000 square feet—has quietly delivered superior performance across virtually every meaningful metric over the recent course of available historical data.

For Basis Industrial, we narrow that definition of Small Bay to properties or portfolios with Multiple Tenancy, where no one tenant makes up more than 10% of the rent roll, and the average size tenant is under 10,000 SFT. We concentrate on the subset of the Small Bay opportunity set most closely aligned with the fundamental factors that underpin the Small Bay thesis – diversity of tenancy and industry, tenant demand, occupancy, manageable leasing capital needs, and retention metrics among others.

This white paper presents an exhaustive analysis of why Small-Bay Industrial represents not only an attractive investment option, but also the single most compelling opportunity in commercial real estate today. Small-Bay is a key source of “alpha” in real estate today and for the foreseeable future. The tailwinds are manifold: vacancy rates half that of larger industrial properties, rent premiums averaging 20% above bulk warehouses, unprecedented supply constraints, and a tenant base so diversified that it provides natural hedging against economic cycles.

Key Investment Thesis Highlights:

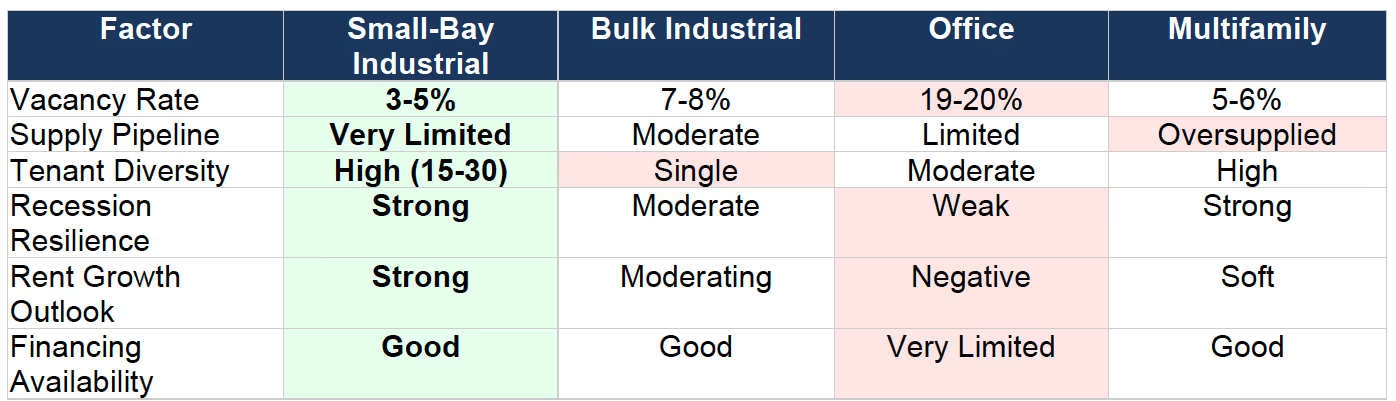

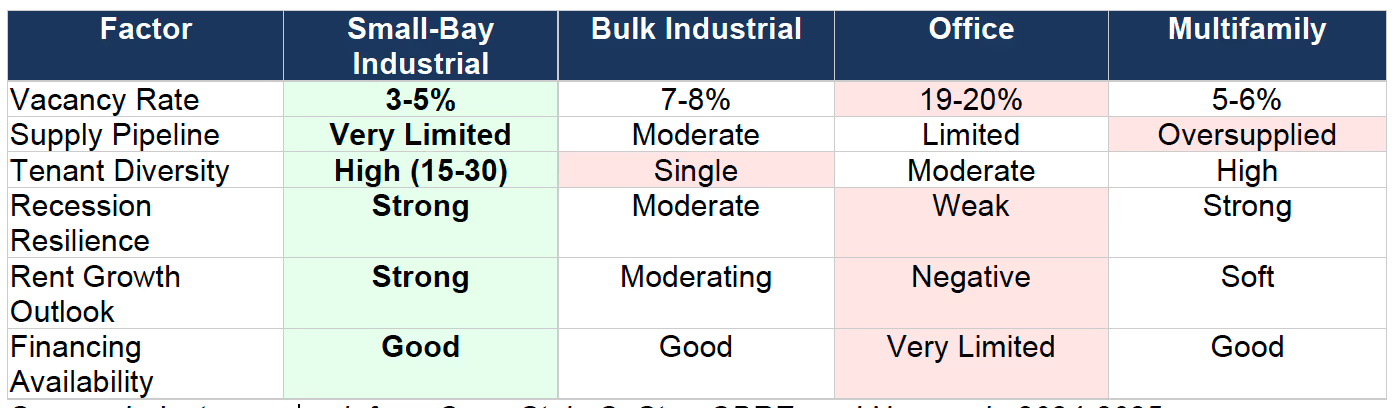

- Vacancy Advantage: Small-bay properties under 50,000 SF show vacancy rates of 3-5%, compared to 7-8% for the broader industrial market

- Supply Scarcity: Only 0.5% of existing small-bay inventory is currently under construction, the lowest in decades, and there are no signs of this changing.

- Rent Premium: Small-bay commands 20-22% higher rents per square foot than bulk industrial.

- Recession Resilience: Diversified tenant base provides natural economic hedge, unavailable in single-tenant properties

- Necessity-Based Demand: Regional, service-oriented tenants serving a customer base that requires them to be proximate to the population centers

- Entry Accessibility: Average acquisition cost of $160/SF versus $320/SF for large-format facilities in premium markets

Understanding Small-Bay Industrial Real Estate

The Basis Way to Go Small

Definition and Characteristics

Small-bay industrial properties—also referred to as shallow-bay, light industrial, multi-tenant industrial, service industrial, or flex industrial—represent a distinct subsector within the broader industrial real estate category. These properties are characterized by several defining features that distinguish them from their larger counterparts:

Building Size: Total building footprints typically range from 20,000 to 200,000 square feet, with individual tenant suites ranging from 1,000 to 10,000 square feet. This configuration allows for multi-tenancy, creating natural diversification within each asset.

Physical Configuration: Small-bay properties feature lower ceiling heights (typically 12-24 feet clear versus 30-40+ feet in modern bulk distribution), higher office-to-warehouse ratios (often 25-50% office buildout), and flexible layouts adaptable to various uses including light manufacturing, assembly, distribution, showroom, destination retail, and service operations. This higher office to warehouse ratio also allows small business owners to house all operations under one roof. Also, whereas traditional office users can work remotely with relative ease, small bay office users are nearly always in-person roles that simply cannot be performed offsite.

Location Profile: These properties predominantly occupy infill locations within established urban and suburban markets—often referred to as "last-mile" or “urban-infill” positions. Their proximity to population centers, labor pools, and end consumers makes them irreplaceable components of modern supply chain infrastructure.

Tenant Profile: The tenant base spans an extraordinarily diverse range of businesses: HVAC contractors, plumbing companies, electrical contractors, auto repair and restoration shops, light manufacturers, food distributors, Co-Packers, medical equipment suppliers, e-commerce fulfillment operators, building materials suppliers, destination retailers, and countless other essential service providers that form the backbone of local economies.

The Market Landscape in 2025

The current state of small-bay industrial real estate presents a compelling picture of supply-demand imbalance that strongly favors property owners and investors. Recent data paints a stark contrast between this subsector and the broader industrial market:

The Strategic Advantages of Small-Bay Industrial

1. Unparalleled Supply-Demand Dynamics

The fundamental driver of small-bay industrial's outperformance lies in an extreme and persistent supply-demand imbalance. While the pandemic era saw developers rush to construct massive distribution centers to accommodate e-commerce growth, the small-bay segment was largely overlooked.

Currently, under 50 million square feet of small-bay industrial space is under construction nationwide, representing less than 0.5% of existing stock. This figure has declined continuously since interest rates rose from historic lows in early 2022. Construction costs during the same time period have rose by over 45%, making new small-bay development economically impossible in most markets, especially in urban in-fill markets where land costs have continued to also rise.

The result is predictable: vacancy rates for properties under 50,000 square feet hover between 3% and 5%, roughly half the vacancy rate of the broader industrial market. In some of the tightest markets, vacancy for small industrial spaces has fallen below 2.5%, with new projects reaching full occupancy within weeks of delivery and existing properties having waiting lists for spaces that will possibly become available.

2. Tenant Diversification: The Built-In Insurance Policy

Perhaps the most compelling structural advantage of small-bay industrial is its inherent tenant diversification. A typical 100,000 square foot multi-tenant small-bay property might house as few as 12 but as many as 40 different tenants across a wide spectrum of industries: contractors, light manufacturers, distributors, service providers, and local businesses that form the essential fabric of regional economies.

This diversification provides multiple layers of protection unavailable in single-tenant properties. No single tenant typically represents more than 5-10% of total rent roll, meaning that even multiple simultaneous tenant defaults would not materially impair property cash flows. The small business tenants who occupy these spaces often cannot easily relocate—their equipment is installed, their customer relationships are local, and their operations are integrated into the community.

Historical performance during economic downturns validates this thesis. During the Global Financial Crisis and the COVID-19 pandemic, multi-tenant small-bay industrial properties maintained significantly higher occupancy rates and rent collection compared to single-tenant facilities, where a single corporate decision to consolidate or close could eliminate 100% of a property's income overnight, and with potential knock-on effects to that company’s nearby suppliers, vendors, customers, and other neighboring businesses weighing on the broader submarket.

3. Superior Inflation Protection

The shorter weighted average lease terms characteristic of small-bay industrial—typically 3-5 years versus 5-10 years for bulk distribution—provide a powerful mechanism for capturing inflationary rent growth. When market rents are rising, shorter lease terms allow landlords to mark rents to market more frequently, accelerating income growth and property value appreciation.

This dynamic proved particularly valuable during the post-pandemic period when industrial rents surged. Properties with shorter lease terms captured these increases rapidly, while owners of single-tenant properties with long-term leases locked in below-market rents watched helplessly as their below-market contracts prevented participation in the market's appreciation.

4. Irreplaceable Infill Locations

Small-bay industrial properties predominantly occupy infill locations within established urban and suburban markets sites that simply cannot be replicated. These "last-mile"/ “urban in-fill” locations provide proximity to population centers, labor pools, and end consumers that is increasingly valuable in an economy demanding faster delivery times and more responsive service.

Land scarcity in these locations creates a permanent barrier to new competition. While a developer might construct a new 1 million square foot distribution center on the urban fringe, finding 5-10 acres of appropriately zoned infill land for small-bay development is exponentially more difficult. This scarcity ensures that existing small-bay properties will continue to command premium rents and maintain high occupancy regardless of overall market conditions.

5. E-Commerce and Last-Mile Logistics Tailwinds

The structural growth of e-commerce continues to drive demand for small-bay industrial space. Industry research indicates that for every $1 billion increase in e-commerce sales, approximately 1.2 million square feet of industrial space is required. The global last-mile delivery market, valued at approximately $175 billion in 2025, is projected to grow to over $375 billion by 2033—a compound annual growth rate approaching 10%.

Mobile commerce alone is projected to account for nearly 59% of total e-commerce sales, with mobile retail traffic representing 77% of global online retail visits. This explosive growth drives demand for small-bay facilities that are positioned close to consumer populations, where orders can be processed and delivered within hours rather than days.

6. Onshoring and Manufacturing Renaissance

Global supply chain disruptions and geopolitical tensions have accelerated a fundamental reshoring of manufacturing to the United States. Government incentives including the CHIPS Act and Inflation Reduction Act have catalyzed billions of dollars in domestic manufacturing investment. This manufacturing renaissance creates a "halo effect" that boosts demand for nearby small-bay industrial spaces—the facilities where component suppliers, service providers, and supporting businesses locate to serve major manufacturing operations.

Small-Bay Industrial vs. Alternative Real Estate Investments

To fully appreciate the investment thesis for small-bay industrial, it is essential to compare this asset class against the primary alternatives available to real estate investors. Each sector presents distinct risk-return profiles, and the comparison overwhelmingly favors small-bay industrial for investors seeking stable, growing income with downside protection.

Versus Office Real Estate

The office sector has experienced unprecedented disruption since 2020. National office vacancy rates reached a record 19.6% in Q1 2025—the highest ever recorded. Remote and hybrid work arrangements, adopted by 72% of office tenants, have fundamentally altered demand patterns in ways that may never fully reverse.

CMBS office delinquency rates have soared to 11.01%, while nearly $950 billion in commercial real estate mortgages—heavily concentrated in office—mature in 2025 alone. Bank lending for office properties has declined 65% from pre-pandemic averages. The contrast with small-bay industrial, where vacancy rates are one-quarter those of office and financing remains available, could not be transparent.

Versus Retail Real Estate

While well-located retail properties—particularly grocery-anchored centers—have demonstrated resilience, the sector faces permanent structural headwinds from e-commerce growth. The same e-commerce expansion that pressures traditional retail simultaneously drives demand for small-bay industrial space for fulfillment and distribution.

Retail real estate also carries concentrated tenant risk. The bankruptcy of a single anchor tenant can devastate an entire shopping center's economics and create cascading co-tenancy issues. Small-bay industrial's diversified tenant base provides protection unavailable in retail formats dependent on one or two major tenants. Small Bay has also siphoned off demand from “destination retailers” whose built-in customer bases will travel to their locations (often in industrial park) making traditional, expensive shopping center locations (with very high CAM) less important to their real estate decision-making

Versus Multifamily Real Estate

Multifamily real estate has attracted enormous institutional capital flows, but this popularity has created challenges. Overbuilding in Sun Belt markets including Austin, Raleigh-Durham, and Nashville has forced property managers to offer significant concessions, with vacancy rates rising and rent growth stagnating in previously high-flying markets.

Regulatory risk also looms larger in multifamily. Rent control legislation, eviction moratoriums, and tenant protection laws can materially impair property economics in ways that simply do not apply to commercial tenancies. Small-bay industrial leases operate under commercial terms with far greater landlord flexibility.

Versus Bulk Industrial/Big Box Distribution

Even within industrial real estate, small-bay substantially outperforms its larger counterparts. Bulk distribution properties over 150,000 square feet face vacancy rates approaching 8%—nearly double that of small-bay. The pandemic-era construction boom delivered unprecedented quantities of speculative large-format space that now struggles to find tenants.

Major corporations including Amazon have scaled back leasing and acquisitions of large distribution space, leaving developers with vacant facilities. In markets like Charlotte, 79% of industrial square footage absorbed in Q1 2024 came from leases under 100,000 square feet, while multiple brand-new 400,000+ square foot big-box facilities sat completely vacant.

Single-tenant bulk distribution also concentrates risk in ways that small-bay avoids. When a major logistics company decides to close or relocate a distribution center, the landlord faces years of vacancy and millions in re-tenanting costs. The small-bay multi-tenant structure ensures no single decision can impair a property's fundamental economics.

Asset Class Comparison Matrix

Acknowledging the Challenges

Intellectual honesty requires acknowledging that small-bay industrial investment is not without challenges. However, as we will demonstrate, these challenges are manageable and, in many cases, actually contribute to the asset class's outperformance by creating barriers to entry that limit competition.

Management Intensity

Multi-tenant small-bay properties require more intensive property management than single-tenant bulk distribution facilities. Managing 15-30 tenant relationships, coordinating maintenance, addressing tenant concerns, and handling lease negotiations require dedicated personnel and systems.

The Counterargument: This management intensity creates a barrier to entry that has historically kept institutional investors away from the sector, allowing better-capitalized operators to acquire properties at more attractive valuations. Those investors who develop operational excellence in managing small-bay properties create sustainable competitive advantages that translate into superior returns. Furthermore, property management technology has advanced substantially, with modern platforms enabling efficient oversight of complex multi-tenant portfolios.

At Basis we are a completely vertically integrated development, property management & leasing platform. This vertical integration allows us to tackle the operational difficulties and excel in this space, while we institutionalize the tenant experience and reporting.

Tenant Credit Quality

Small-bay tenants are predominantly small and medium-sized businesses without the investment-grade credit ratings of major corporations. This creates perceived credit risk that some institutional investors find uncomfortable.

The Counterargument: The diversification inherent in multi-tenant small-bay properties superior credit protection compared to single-tenant properties with investment-grade tenants. When Amazon or Walmart decides to close a distribution center, the landlord faces years of vacancy. When one of 25 tenants in a small-bay property fails, the impact on total income is minimal and the space can typically be re-leased quickly given persistent demand. Historical data shows that multi-tenant light industrial properties have maintained higher occupancy and rent collection through economic downturns than single-tenant facilities.

We have come up with novel approaches to enhance or at least vet tenant credit worthiness. All our tenants who cannot provide full financial packages for review, are required to apply and pay for a full background check and credit report for themselves and their business. After these reports are received we increase their security deposit depending on results.

Transaction Size Limitations

Individual small-bay properties represent smaller transaction sizes than bulk distribution acquisitions, making it more challenging for large institutional investors to deploy significant capital efficiently.

The Counterargument: This limitation has historically resulted in more attractive acquisition pricing for small-bay properties. The lack of institutional competition meant that small-bay traded at 50-100 basis point cap rate premiums to bulk distribution. This dynamic is now reversing as sophisticated investors recognize the asset class's fundamental strengths, but opportunities remain for investors willing to aggregate portfolios through individual acquisitions.

Current Market Correction

Following peak pricing in 2022, some small-bay markets have experienced price corrections as interest rate increases have affected valuations across all real estate asset classes. Some owners who acquired properties at peak pricing face challenges.

The Counterargument: Price corrections create buying opportunities for well-capitalized investors. Properties purchased at current valuations can withstand market fluctuations and provide negotiating flexibility. Distressed sales provide entry points at attractive basis, and the fundamental supply-demand dynamics that drove small-bay's outperformance remain intact. The current environment favors disciplined acquirers over speculative buyers.

Regional Market Dynamics

While small-bay industrial fundamentals are strong nationally, certain regional markets offer particularly compelling opportunities based on population growth, supply constraints, and economic diversification.

Sun Belt Markets

Markets including Dallas-Fort Worth, Phoenix, Las Vegas, Atlanta, Central, and South Florida continue to benefit from population migration and business relocation trends. Strong population growth drives demand from contractors, building suppliers, and service businesses that require small-bay space to serve expanding communities. Light industrial suites under 30,000 square feet in secondary markets saw rent growth of over 5.9% annually—more than triple the rate in the most expensive coastal markets.

Midwest Stability

Markets like Chicago, Columbus, Indianapolis, and Kansas City offer steadier performance with less volatility. Strong manufacturing bases, strategic logistics positioning, and stable population provide consistent demand. These markets may not experience the dramatic rent growth of Sun Belt markets, but they also avoid significant corrections, providing reliable cash flow for income-oriented investors.

Tight Coastal Markets

High-barrier coastal markets including Southern California, the San Francisco Bay Area, Northern New Jersey, and South Florida feature the tightest supply conditions. Land constraints make new development nearly impossible, ensuring that existing small-bay properties will maintain their value indefinitely. While rent growth has moderated in these markets, the irreplaceable nature of infill locations provides exceptional downside protection.

Conclusion: The Case for Going Big in Small Bays

The evidence presented in this white paper leads to an inescapable conclusion: small-bay industrial real estate represents the single most compelling investment opportunity in commercial real estate today. The combination of structural supply constraints, diversified tenant demand, inflation protection, recession resilience, and secular tailwinds from e-commerce and manufacturing onshoring creates an investment thesis unmatched by any other real estate asset class.

The numbers speak for themselves:

- Vacancy rates far below the level of bulk industrial and one-quarter the level of office

- Construction pipeline at historic lows with no near-term catalyst for change

- Rent premiums of 20%+ over larger industrial formats

- Historical outperformance through multiple economic cycles

- Fundamental demand drivers that will persist for decades

For investors seeking stable income, growth potential, and downside protection, the message is clear: Go Big in Small Bays. This overlooked subsector offers everything sophisticated real estate investors demand—yield, growth, and resilience—in a single package that consistently outperforms its more glamorous competitors.

"Small-bay industrial is not just a niche sector; it's a strategic cornerstone of modern logistics and light manufacturing. The combination of location, flexibility, and tenant diversity makes these properties incredibly resilient and well-suited to today's evolving industrial landscape. Small-Bay also is the lifeblood of the small business entrepreneur in America, they leave their garage, and their first stop is Small-Bay. " Anthony Scavo, Managing Partner – Basis Industrial.

* * *